Table of Content

As long as you lived in the home as your primary residence for two of the last five years before it was sold, you’ll be eligible for this tax benefit. Keep your invoice, receipts and work orders to prove you used your home equity loan funds for home improvements. You’ll receive a closing disclosure three business days prior to closing, which provides a breakdown of all the costs paid when your home was purchased. You should receive a form 1098 from your current loan servicer at the end of the year. The amount listed in Box 1 shows the amount of interest you paid. Forbes Advisor adheres to strict editorial integrity standards.

Finder makes money from featured partners, but editorial opinions are our own. Here’s how that works with a home valued at $400,000 with a loan balance of $300,000. These are significant increases on what the limits were before. Each week, you'll get a crash course on the biggest issues to make your next financial decision the right one. This distinction is important to get straight, particularly since you might have a home equity loan or HELOC that’s not considered home equity debt, at least in the eyes of the IRS.

Acquisition debt vs. home equity debt: What’s the difference?

If your total mortgage debt is higher than that, then you won’t be able to deduct all of the combined interest paid. What’s more, you must spend the money on the property in which the equity is the source of the loan. If you meet the conditions, then interest is deductible on a loan of up to $750,000 ($375,000 or more for a married taxpayer filing a separate return). The funds were used to buy, build or improve a qualifying home.

Leveraging your home’s equity just for the sake of lowering your taxes may not be the best financial choice. You borrowed $100,000 from your home’s equity and used the funds to pay for your child’s college education instead of taking student loans. You cannot take the tax deduction because you didn’t use the funds for a first or second home.

Personal Loan

For example, if you own a home and take out a home equity loan for $100,000 to add a room and prove you used the entire $100,000 for that purpose, you can deduct the mortgage interest paid. Make sure you stay alert as to any tax changes because 2019 will be a landmark year. Many of the provisions set out by the TCJA will be coming into effect for the first time this coming tax filing season. The AMT exemption will be $71,700 for individuals, with a gradual phaseout at $510,300. Married couples filing jointly will see their exemption raised to $111,700, with a phaseout limit of $1,020,600.

If you sell your home, you can deduct your home mortgage interest paid up to, but not including, the date of the sale. If you're married and file a joint return, your qualified home can be owned either jointly or by only one spouse. You don't rent the same or different parts of your home to more than two tenants at any time during the tax year. If two persons share the same sleeping quarters, they are treated as one tenant. If you have a second home and rent it out part of the year, you must also use it as a home during the year for it to be a qualified home.

year HELOC Rates

For this purpose, gross income is all income received during the entire year, including amounts received before the corporation changed to cooperative ownership. If you received a refund of mortgage interest you overpaid in an earlier year, you will generally receive a Form 1098 showing the refund in box 4. Dan paid $3,000 in points in 2011 that he had to spread out over the 15-year life of the mortgage. You must spread any additional points over the life of the mortgage. The buyer reduces the basis of the home by the amount of the seller-paid points and treats the points as if he or she had paid them.

If you’re interested in seeing how much you can borrow with a home equity loan, start an application with Rocket Mortgage® to see if you qualify. If you used the funds to renovate your home, you’d need all receipts for materials, labor and any other costs incurred to renovate the property. Knowing how to deduct home equity loan interest is important. The key is to have proper documentation and to understand the IRS rules.

Enter the result as a decimal amount 14.× .15.Multiply the amount on line 13 by the decimal amount on line 14. A mortgage secured by a qualified home may be treated as home acquisition debt, even if you don't actually use the proceeds to buy, build, or substantially improve the home. Bill deducts 25% ($25,000 ÷ $100,000) of the points ($2,000) in 2022. If you qualify for mortgage assistance payments for lower-income families under section 235 of the National Housing Act, part or all of the interest on your mortgage may be paid for you. If you're a minister or a member of the uniformed services and receive a housing allowance that isn't taxable, you can still deduct your home mortgage interest. You may be able to claim a mortgage interest credit if you were issued a mortgage credit certificate by a state or local government.

You may not immediately receive written communications in the requested language. The IRS’s commitment to LEP taxpayers is part of a multi-year timeline that is scheduled to begin providing translations in 2023. You will continue to receive communications, including notices and letters in English until they are translated to your preferred language. Go to IRS.gov/IdentityTheft, the IRS Identity Theft Central webpage, for information on identity theft and data security protection for taxpayers, tax professionals, and businesses. If your SSN has been lost or stolen or you suspect you’re a victim of tax-related identity theft, you can learn what steps you should take. Go to IRS.gov/SocialMedia to see the various social media tools the IRS uses to share the latest information on tax changes, scam alerts, initiatives, products, and services.

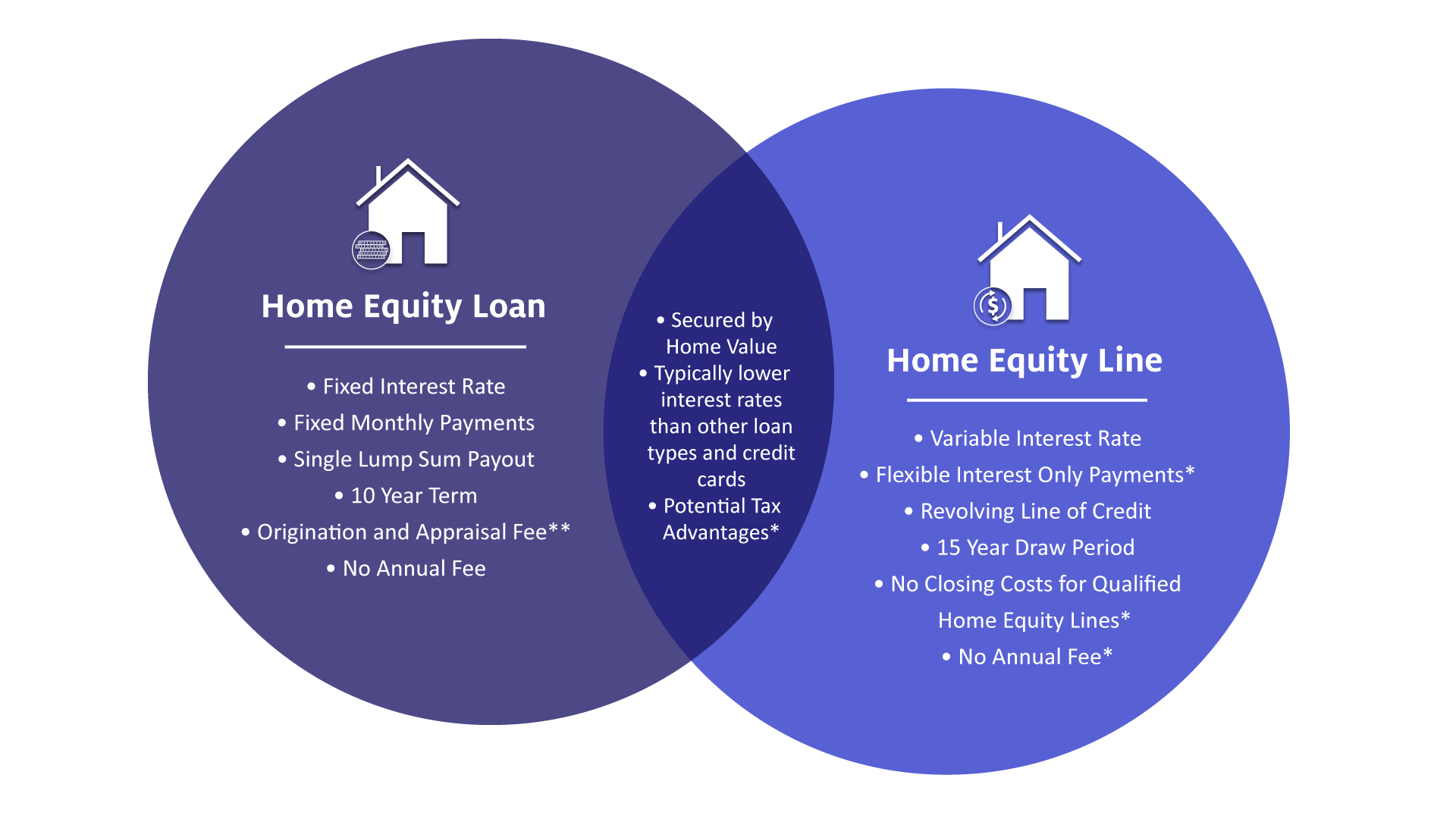

Also, remember that you can’t deduct your home equity loan interest if you take the standard deductions, which are slightly higher in 2021 versus 2020. If you aren’t sure whether to itemize or take the standard deduction, contact a tax professional for guidance. This is the last year you’ll be able to take the residential energy credit. You may be able to get a tax credit equal to 22% to 30% of the improvement costs toward eco-friendly improvements like installing solar panels or energy-efficient appliances. You can leverage the equity in your home with home equity loans, which differ from lines of credit in that they are taken out for a set amount and paid back on a regular basis with a fixed interest rate. You can also look online for rates to compare lenders with your current mortgage lender prior to fully applying for a HELOC.

If you take this credit, you must reduce your mortgage interest deduction by the amount of the credit. If you pay off your home mortgage early, you may have to pay a penalty. You can deduct that penalty as home mortgage interest provided the penalty isn't for a specific service performed or cost incurred in connection with your mortgage loan. If you're married filing separately and you and your spouse own more than one home, you can each take into account only one home as a qualified home. However, if you both consent in writing, then one spouse can take both the main home and a second home into account. You may want to treat a debt as not secured by your home if the interest on that debt is fully deductible whether or not it qualifies as home mortgage interest.

Personal loans are an option if your credit score is good, and you could also charge expenses on a credit card and pay it off over time. But personal loans aren't always easy to qualify for, and credit card debt is generally bad news. That's why you might consider borrowing against your home, provided you have enough equity in it to do so. Not only is that generally an affordable option, but it may offer some tax benefits to boot. If you are improving your property, chances are the interest will be tax-deductible, but check with your accountant to be sure. The improvements need to be made on the property on which you are taking out the home equity loan.

Questions and responses on finder.com are not provided, paid for or otherwise endorsed by any bank or brand. These banks and brands are not responsible for ensuring that comments are answered or accurate. A steady income, more equity and low debt are key to getting approved with bad credit.

Get started by reviewing our list of the best tax software. This tax information is provided for general purposes only and should not be relied on or construed as tax advice. Consult with a qualified tax preparer for more information. Fixed rates are available for home equity loans, allowing homeowners to manage their monthly budgets better. Home equity offerings vary, so reviewing the terms and conditions applicable to the product you’re considering is important. The information in this article is provided to help you better understand these options and may not reflect products or offerings available from AmeriSave.

However, you can't deduct the prepaid amount for January 2023 in 2022. (See Prepaid interest, earlier.) You will have to figure the interest that accrued for 2023 and subtract it from the amount in box 1. You will include the interest for January 2023 with other interest you pay for 2023. In the year paid, you can deduct $1,750 ($750 of the amount you were charged plus the $1,000 paid by the seller). You must reduce the basis of your home by the $1,000 paid by the seller. This reduction results in original issue discount, which is discussed in chapter 4 of Pub.

No comments:

Post a Comment